The energy market is changing rapidly. Oil prices initially rose to $80 to start this year. However, oil quickly reversed the course and plunged into $60 on tariff-driven concerns. Oil prices have bounced off its bottom, but everyone is guessing where the crude prices will go next.

Considering how quickly things change Energy Marketmany companies are taking steps to help them survive the ups and downs of the industry. Chevron (NYSE: CVX), Energy Transfer(NYSE:ET)and exxonmobilI He stands out among the analysts who contribute to several fool.com for their ability to handle anything the market is throwing on. It makes them an ideal option for those looking for attractive and durable dividend income.

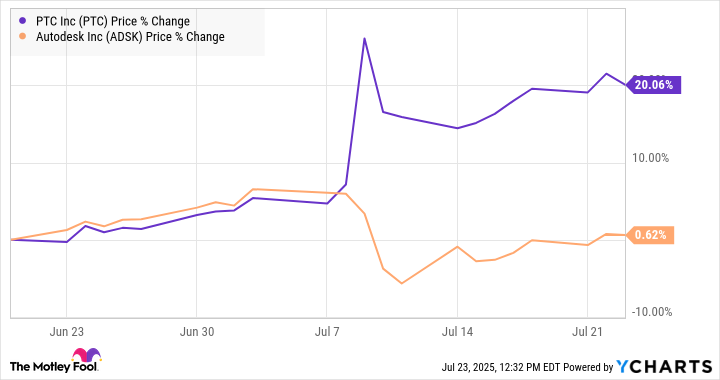

Image source: Getty Images.

Reuben Greg Brewer (Chevron): There is one feature that investors should not overlook about Chevron. It’s a balance sheet. With a debt-to-equity ratio of about 0.2x at the end of the second quarter, it has one of the most powerful financial positions within the integrated energy peer group. In most cases, investors pay more attention to oil prices and geopolitical events than to balance. However, Chevron’s ability to survive the path is partly linked to its financial strength.

Chevron, for example, completed the acquisition of Hess for around $53 billion. In order to inject trades on that scale, you need both size and financial strength. But here’s something interesting. The transaction was agreed in October 2023! The deal was stuck in court due to Hess’s relationship with Chevron’s peers. As far as Chevron did, few companies could afford to stick, no matter how attractive the deal was. And the strength of the energy giant’s balance sheet was a key factor in the trade’s resilience to headwinds they faced.

But that’s not the only place where a strong balance sheet is a big profit. Oil prices are very unstable, leading to shaking of materials at the top and bottom lines of companies like Chevron. Still, Chevron has been able to increase its annual dividend for the 38th consecutive year. how? You have the ability to add debt during difficult times, and you can be confused until a good time comes back (at which point you can reduce leverage again).

With an attractive 4.7% dividend yield, even conservative investors should appreciate Chevron’s ability to survive all the storms that have arrived over 38 years.

Neha calls(Energy Transfer): These are challenging times to become investors in the energy sector. Oil prices are volatile and the global energy environment is changing in favour of cleaner energy sources. However, unlike crude oil and coal, demand for natural gas is expected to rise steadily over the next few decades, especially driven by an increase in demand for electricity.

Given the dynamics, stocks like energy transfer not only can survive in today’s changing landscape, but will thrive in the long term. This is because energy transfer is a large natural gas player that generates stable cash flow and pays large dividends.

Energy Transfer operates a pipeline of over 130,000 miles. More than 50% of the $5 billion projected growth capital expenditure for 2025 will be spent on expanding natural gas pipelines and natural gas liquid capacity. It also builds eight natural gas fire power plants to support its operations in Texas. The company recently won its first commercial transaction to supply natural gas to its Texas data center.

Therefore, energy transfer has a strong growth catalyst and economic fortitude to support growth plans. The company also pays a stable dividend and aims to grow annual dividends of 3% to 5% over the long term. Combined with a high yield of 7.4%, energy transfer stocks are today a compelling purchase case.

Matt Dillallo (Exxonmobil): Exxonmobil has built its business not to survive, but to thrive in the rapidly changing energy market. Energy giants have an unparalleled global portfolio of low-cost upstream oil and gas production assets complemented by major product solutions businesses (refining, chemicals, specialty products). Exxon is also building a growing low carbon solution business.

These businesses offer strong and growing revenues in the face of ongoing product price volatility. For example, last year was Exxon’s third most profitable year in the last decade, despite commodity prices hovering towards the low end of the historic range.

The company’s growing scale gives it a great competitive advantage and allows it to take advantage of its scale to reduce costs. Since 2019, Exxonmobil has achieved $12.1 billion in annual cost reductions, with IT reaching $18 billion in total annual cost reductions by 2030. These ongoing cost reductions will further strengthen the changing weather in the oil market.

Exxon also boasts one of the most powerful balance sheets in the energy sector. This gives you the flexibility to borrow money during periods of lower oil prices and allows you to continue growing. If the product price improves, we will repay the debt.

The combination of low cost, scale and balance sheet strength from oil giants places dividends (over 3.5%) on a highly sustainable foundation. The oil giant has increased its payments for the 42nd year in a row. S&P 500.

Exxon expects to achieve revenue growth of $2 billion and cash flow growth of $300 billion by 2030. These targets represent combined annual growth rates of 8% revenue and 10% cash flow based on the average oil price per barrel below current market levels. This will provide enough fuel to the oil giant and allow the high-revenue dividends to continue to increase.

This combination of financial strength and visible growth puts ExxonMobil in a superior position in today’s changing energy market.

Consider this before purchasing stock at Chevron.

Motley Fool Stock Advisor The analyst team has identified what they believe 10 Best Stocks For investors to buy now…and Chevron was not one of them. The 10 stocks that have made the cut could potentially generate monster returns over the next few years.

When should you think about it? Netflix I created this list on December 17, 2004…If you invested $1,000 at the time of recommendation, There is $636,628! *Or when nvidia I created this list on April 15, 2005… If you invested $1,000 at the time of recommendation, There is $1,063,471! *

Now it’s worth noting Stock Advisor The total average return rate is 1,041% – Outperformance that breaks the market compared to the 183% of the S&P 500. Don’t miss the latest Top 10 list and get it when you join Stock Advisor.

Matt Diallo There are positions in chevrons and energy transfer. Neha calls There is no position in any of the stocks mentioned. Reuben Greg Brewer There is no position in any of the stocks mentioned. Motley Fools holds a job and recommends Chevron. To Motley’s fool Disclosure Policy.