Financial technology, or fintech, is the innovating and finding new ways to drive money between people and businesses. PayPal(NASDAQ: PYPL) This is the original Fintech stock. It has been around since 2000 and survived the infamous dot-com bubble. Today, it is known for its digital and mobile payment network of the same name and for its peer-to-peer payment app Venmo.

Unfortunately, PayPal is no longer hot. The business is old and stocks have fallen almost 80% from the 2021 high. PayPal’s new CEO, Alex Chriss, is hoping to teach the old company new tricks to bring back brands and stocks.

Can I buy PayPal today? Fintech Stock Have you seen that best day?

The answer may surprise you.

Although not flashy, PayPal is even more prominent in the field of fintech than you would guess. The company’s payments ecosystem spans approximately 434 million active accounts across 200 markets, processing $1.68 trillion in payments last year. Establishing a global payment network is extremely difficult in the face of competition and regulatory hurdles.

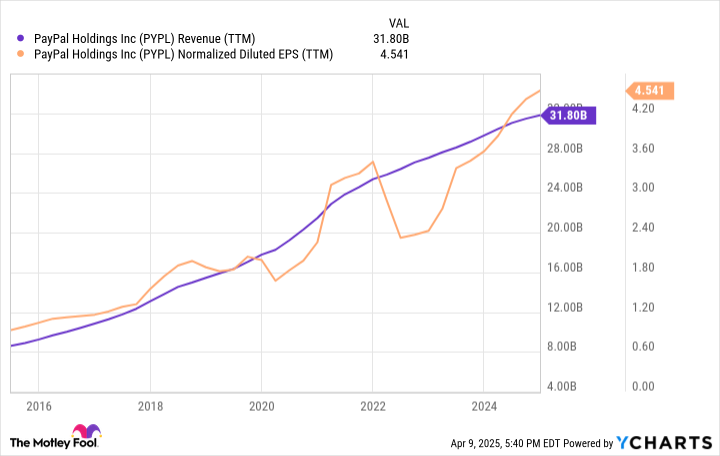

Has PayPal’s business been outdated? I would say that. The margins are steadily eroding due to competition in payment processing businesses. Company’s Total margin I slid from about 64% 10 years ago to less than 46% at the beginning of last year. Furthermore, active accounts have been stagnant since 2021.

These are two nightmare developments! However, PayPal continues to expand its top and bottom lines.

This is how you stumble and you can’t increase your earnings per share over the course of 10 years. If the core business is good, what will happen when Chriss executes his plan to build new products and features?

At a recent investor event, PayPal highlighted its goal of becoming a commercial platform. We want to leverage payment technology and user data to drive engagement between users and merchants. In other words, PayPal wants a platform that encourages people to buy, sell, pay and borrow, which is beneficial to more people.

This takes time, but the company has a high ceiling if executed well. PayPal’s network helps you compete in emerging vertical markets, including peer-to-peer payments, BNPL (buy now, pay later), business loans and services. We launched a new digital advertising segment just a few months ago.

PayPal led revenue growth of 6% to 10% in 2025, achieving low teenage growth by 2027, and an annual revenue growth of at least 20% since. That’s an aggressive goal, but again, PayPal’s revenue has almost quadrupled over the past decade, despite the margins collapse and little unified among the company’s moving parts.

The best opportunity allows you to make money without going everything the way you want when you have far more rewards than risk. I think this applies to PayPal here.

There’s no bones about it: PayPal has become a value stock. Stocks are trading at the lowest valuation on record. This includes a price (P/E) ratio of just 16 and free cash flow yields above 10%. I don’t know if there are other stocks with such a low rating, but I have a shot with a long-term revenue growth rate of 20% per year.

Additionally, PayPal announced a new $15 billion repurchase program in the fourth quarter. In combination with the rest of the existing program, this brings PayPal’s future total buyback to nearly $20 billion. This is about one-third of the market capitalization. Management is to put that money in their mouths and act on the value it sees.

Massive repurchases can help you collapse stock numbers, increase your finances per share, and establish a higher floor of stock. Plus, PayPal can afford it. The company already owns $10.8 billion in cash and is expecting cash flows of between $6 billion and $7 billion this year. If PayPal doesn’t organically achieve its growth target, it’s a financial buttless.

As you would like, PayPal’s market capitalization is almost $60 billion. That’s probably too big for a small investment to grow into a big money.

However, PayPal can reward patient investors with investment returns that will win the market for years if they endure that possibility. Yes, it helps to move the needle and lift a diverse portfolio. Buying a high quality and growing business with a Dirt cheap rating is a victory strategy that can set you up for life over time. PayPal is a strong candidate that suits that type.

Consider this before purchasing inventory with PayPal.

Motley Fool Stock Advisor The analyst team has identified what they believe 10 Best Stocks For investors to buy now…and PayPal was not one of them. The 10 stocks that have made the cut could potentially generate monster returns over the next few years.

When should you think about it?NetflixI created this list on December 17, 2004…If you invested $1,000 at the time of recommendation,There is $495,226! * Or when nvidiaI created this list on April 15, 2005… If you invested $1,000 at the time of recommendation,There is $679,900! *

Now it’s worth notingStock AdvisorThe total average return rate796% – Market-breaking outperformance compared to155%For the S&P 500. Don’t miss out on the latest Top 10 list that you can use when participatingStock Advisor.

Justin Pope There is no position in any of the stocks mentioned. Motley Fool has a position and recommends PayPal. Motley Fool recommends the following options: $42.50 calls for length PayPal in January 2027 and $77.50 calls for short $77.50 PayPal in June 2025. To Motley’s fool Disclosure Policy.