These two momentum stocks got a bullish nod – this is why they can reach the new best

Buying on rising stocks is a natural impulse and a viable investment strategy. Momentum investment is a technology that detects and tracks upward trends in the market, as it is called.

Of course, every investment style has boosters and bummers, and both sides usually have strong arguments in their favor. Remember that the key to success is finding balance, and past performance doesn’t guarantee future returns, but it can provide useful indications of where your inventory is heading.

With that in mind, jump into the momentum stocks that are currently attracting investors’ attention. Using Tipranks Databasefocusing on two names that not only recently won steam, but also received bullish support from at least one street analyst. Let’s take a look.

Bridgebi Offerma(bbio))

The first momentum stock on our list today is BridgeBio, a biopharmaceutical company focusing on rare and serious genetic diseases. More specifically, BridgeBio selects disease targets with what is called “clear genetic factors.” In other words, we are developing drug candidates to treat diseases that are genetically associated with a single mutation. BridgeBio has chosen a wide range of functions, as it offers a choice of over 10,000 genetic diseases that meet target criteria. More importantly, BridgeBio is given plenty of openings because the group of this disease has relatively few FDA-approved drugs.

BridgeBio is based on its development work based on its own drug development platform, creating new drugs to look for new genetic diseases to target, address symptoms, and improve patient outcomes. The company follows this development stage, commercialising is the ultimate goal by moving drug candidates from a successful clinical trial series into a regulatory process. Bridgebio reached that goal late last year.

Last November, the company received FDA approval for its drug Acoramidis for the treatment of cardiomyopathy in wild-type or mutant transthyretin-mediated amyloidosis (ATTR-CM), a disease that affects the myocardium. Treatment with Akoramidi was shown in clinical trials to reduce disease deaths and hospitalizations, with statistically significant improvements in patients undergoing treatment. BridgeBio is selling new drugs under the brand name Attruby, with 1Q25 being the first quarter of the company’s commercialization efforts. The company is investigating akoramidis in its clinical trial program. There, the subject of phase 3 conduct studies, testing whether it helps prevent the development of active disease in asymptomatic patients carrying pathogenic TTR variants.

Looking at the company’s financial side, we found that BridgeBio’s 1Q25 revenue release showed $116.6 million in total revenue. The company’s revenue balance was derived from the revenue from licenses and services. Compared to the previous year’s quarter, this segment of revenue fell by $131.2 million, with a 45% decline in total revenue from the previous year, but in reality, the total distance was $58 million with Atturby’s superior debut support. Bridgebio had a net loss of 88 cents per share in the quarter, which was 5 cents per share than expected. Investors like the story here, with stocks showing strong profits year-over-year.

Bridgebio is attracting attention from Oppenheimer Analyst’s Trevor Allred, who has taken a more bullish stance on stocks in light of Attruby’s successful commercialization. Allred writes: “I’ve been wrong with Bbio since its inception. Bridgebio’s team has successfully carried out the launch of Attruby, and the stock is considered a commercial outperformance and clinical catalyst in YE. To exacerbate by positive clinical results from clinical trials of ADH1 and LGMD2I around YE.

Allred follows these comments and is a $60 price target, meaning an upgrade from performance (i.e. neutral) to BBIO rating (i.e. buy) and a one-year upside potential of 26%. (To see Allred’s achievements, click here))

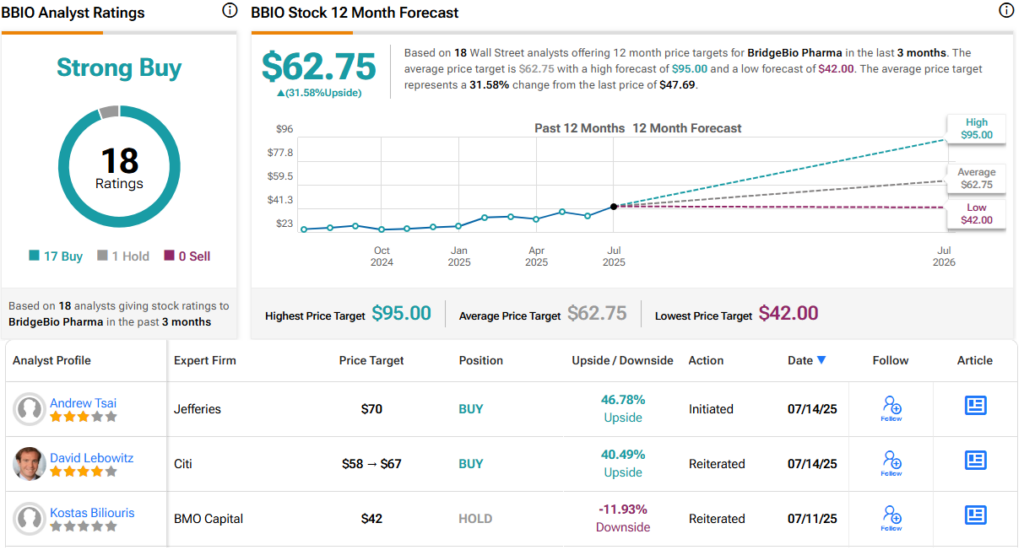

Overall, the stock has earned a strong buying consensus rating from the streets based on 18 recent reviews, with a biased collapse of 17 buisses. The stock price is $47.69, with an average target price of $62.75 suggesting that the stock price will increase by 31.5% next year. (look BBIO Stock Prediction))

So-Young International(and))

Next on the list of stocks with momentum is So-Young, a Chinese company. A company that operates a social media platform that links the medical aesthetic industry and connects the various consumers, professionals and health service providers in the aesthetic sector. The platform makes reliable and reliable information available about the carefully reviewed and curated networks of medical aesthetic providers. The service platform focuses on content delivery in China, leveraging major social media networks and other target media platforms.

Social media and medical aesthetics are both growing industries, and So-Young builds brand images based on user trust, broad reach and valuable data insights. So-Young’s user base allows you to trade information with clinics, latest treatment trends in aesthetics, and quality of treatment, all allowing better patient decisions. The company is working to expand its network, adding medical areas such as dentistry, dermatology, ophthalmology and basic physical examinations. The service focuses on China and the company is based in Beijing.

In the 1Q25 financial release, So-Young reported significant benefits in the number of active users on its network and the number of paid visits verified. Active users are defined as those who have visited Aesthetic Clinic at least once in the last 12 months, totaling over 75,500, with a significant profit from 8,000 reported in the previous year. The profits from the verified paid visits were similar, with 45,500 in 1Q25 compared to 4,600 in 1Q24. The company reported first quarter revenues at the high end of the previously published guidance range, compared to RMB3118.3 million for the first quarter of 2024.

The stock has grown 411% this year, a large portion of the profits it has generated over the past month, and this China’s momentum inventory has attracted the attention of city analyst Nelson Chung, who was impressed by the company’s recent growth. Cheung said of So-Young and its outlook: “Since its launch in November 2024, Soyoung Clinic has rapidly expanded at 31 centers in Jun’s metropolis (Beijing, Shanghai, Deutshenzhen), and has examined the strength of SY in 1); Cross-selling 2027e for accurate targeting and site selection.” (To see Cheung’s track record, click here))

Looking at it, Cheung valued the stock as a buy and achieved its price target of $5.50, suggesting a one-year profit for the 30% share. Cheung’s is the only analyst review on this stock file and is currently trading at $4.24. (look sy stock prediction))

To find good ideas for stocks to trade with attractive ratings, check out Tipranks Best stocks to buya tool that combines all Tipranks’ fairness insights.

Disclaimer: The opinions expressed in this article are those of featured analysts. Content is intended for informational purposes only. It is very important to do your own analysis before making an investment.