TSMC stock maintains high conviction AI play status with a price target of $220

Taiwan semiconductor Manufacturer (TSM), or TSMC for short, is the world’s Numero UNO Pure-Play Semiconductor Foundry, which has skyrocketed nearly 20% over the past month. Despite this impressive gathering, my outlook remains bullish.

The company is well suited to benefit from strong tailwinds, including relentless AI-driven demand, a dominant, frequently exclusive position in advanced chip manufacturing, continuous geographic diversification, and stable cadence of technological breakthroughs.

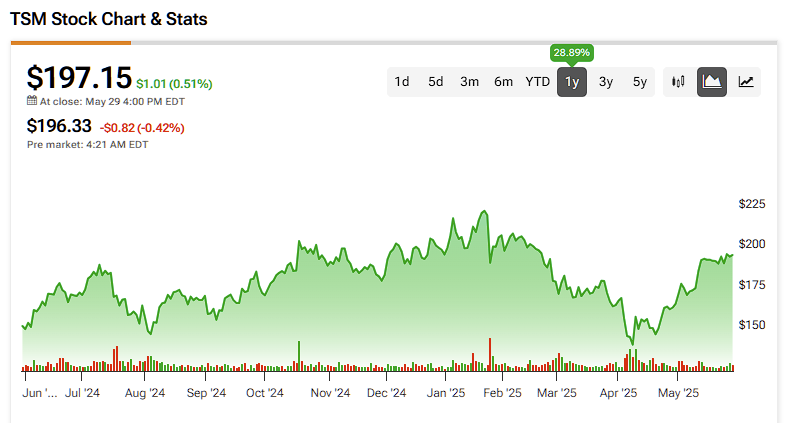

TSMC (TSM) stock history for the past 12 months

TSMC continues to be a major manufacturer and a major supplier of major chips ai Power plants including NVIDIA (NVDA), Advanced Micro Devices (AMD), Apple (AAPL), and Qualcomm (QCOM). In particular, TSM is also a producer of Nvidia’s. The cutting edge blackwell chip serieshas become extremely popular recently.

TSMC’s 3NM process currently represents the most advanced semiconductor technology in the industry, offering superior power efficiency and performance. Future forecasts are built around the upcoming 2NM and 1.6nm nodes of the company, which are scheduled for release in the second half of 2025 and 2026, respectively.

The 2NM technology, called N2, remains on good track record for volume production in the second half of 2025. This next-generation process is expected to improve processing speeds by 10-15% with the same power consumption, or reduce power usage by 20-30% with comparable performance. Following this, the 1.6NM process is predicted to further improve power efficiency by 15-20% over the 2nm node.

TSMC (TSM) Revenue, Revenue, Profit Ratio History

These advances are particularly timely as data centers are tackling rising energy costs. The shift to more power-efficient chips is becoming more economical than just a technical mandate. This positions TSMC as a key enabler of the ongoing global semiconductor upgrade cycle.

Reflecting this momentum, TSMC outlined strong long-term growth expectations. The company forecasts its AI-related chip revenue to grow at a combined annual growth rate (CAGR) of 45% over the next five years, but overall revenue is projected to grow at a CAGR of 20% over the same period. These figures highlight the company’s pivotal role in driving the future of computing.

This growth potential has not been overlooked. Famous Investors Cathy WoodThe ARK Fund recently purchased 241,047 Taiwanese stocks worth $46.3 million.

TSM commands an overwhelming 64.9% global market share in the foundry segment, and warns its closest competitors, Samsung Electronics (SMSN) and Intel (INTC). Politician. Its unparalleled scale, deep client relationships, and technical edge create a formidable barrier to entry.

This dominant position grants TSM the key pricing power. Clients, which many have relied on TSM for decades, are unlikely to switch suppliers as they risk falling behind in the rapidly evolving AI race.

One of the major risk factors associated with TSM is Taiwan’s geographical location, poses the risk of a Chinese acquisition. However, TSM is actively tackling these risks by prioritizing geographic diversification as its core strategic initiative and diversifying its global manufacturing footprint.

In addition to a $65 billion investment in US-based Fab, TSM has pledged an additional $100 billion to expand its capabilities around the world. The Arizona facility is reportedly operating at full capacity until 2027, highlighting robust demand. This geographic diversification not only reduces exposure to potential tariffs, but also strengthens TSM’s resilience to geopolitical volatility.

Beyond the US, TSM is also established. New Chip Design Center Manufacturing factories in Munich, Germany, Dresden, Germany, and new fabs in Japan. Strategic investment beyond the home base of Taiwanese semiconductors reflects wise risk management and strengthens the strategic change to a more balanced global presence.

TSM is set to report second quarter revenue on July 17th. The company is projected to report earnings per share (EPS) of $2.30, representing a 57.5% increase from the previous year. Additionally, second quarter revenue is projected to increase by 13% year-on-year, ranging from $28.4 billion to $29.2 billion due to high demand for advanced 3 nanometers (nm) and 5 nm processes.

On May 9th, TSM announced its impressive return rate for April 2025, showing the highest ever in the company’s history. Net revenue for April galloped from 48.1% year-on-year to 349.6 billion units (approximately $11.6 billion). It is noteworthy that TSM forecasts sales growth of 24% to 26% in 2025, due to strong demand for the latest nanokip amid the surge in AI.

TSMC (TSM) Revenue History

Importantly, TSM trades with attractive ratings compared to their peers. As for ratings, TSM looks cheap. Currently trading at an attractive forward P/E ratio of 21 times compared to the much higher multiples of the peer group. Semiconductor Company Advanced Micro Devices trades at a higher forward P/E multiple (28X), while AI Prodigy Nvidia trades at a 32X forward P/E.

TSMC (TSM) Peer Comparison

On Wall Street, TSM stock has a strong buy consensus rating based on seven buys, one hold and zero sales ratings over the past three months. TSM’s average stock price target is $219.43 It means about 11% upside potential over the next 12 months.

The semiconductor industry continues to continue strong growth, driven primarily by rapid adoption. artificial intelligence technology. With its unparalleled manufacturing capabilities, deep-built customer relationships and a sophisticated technology roadmap, TSMC is positioned very well to take advantage of this transformative trend.

The company’s timely investment in next-generation nodes (particularly 2nm and 1.6nm) is in good agreement with the growing demand driven by the wider upgrade cycles across the technology environment, along with its global manufacturing expansion. These factors make TSMC a collectively compelling long-term investment opportunity. With a lucrative valuation and strong revenue momentum, the current environment offers an attractive entry point for investors looking to gain exposure to accelerated AI megatrends.